Indian professionals who are moving back from the United Kingdom often lack clarity about how they can manage their overseas holdings like stocks, ETFs, Individual Savings Accounts (ISAs), and workplace pensions after moving back.

This article explains how you can manage your overseas holdings after moving back to India. We cover your new Indian tax and reporting requirements, what happens to the tax-free status of your ISA, how to handle your SIPP or workplace pension, and how you can use RNOR rules to optimize your transition.

Table of contents

- What happens to my stocks when I move back to India?

- What happens to my ISA when I move back to India?

- What happens to my UK Pension (SIPP or Workplace) when I move back?

- Will I be subject to UK Inheritance Tax after moving back to India?

- Tax and reporting implications of moving back to India

- What is RNOR status and how does it affect me?

- Common Questions UK NRIs Have About Moving Back

- About Paasa

What happens to my stocks when I move back to India?

Under Indian FEMA regulations, you are legally allowed to indefinitely hold any foreign stocks or ETFs you acquired while living in the UK. You do not have to sell them just because you moved.

However, while Indian law allows you to keep them, UK platforms might not:

- Retail Fintechs (Trading 212, Freetrade, Plum): These platforms generally cater strictly to UK and EEA residents. If you update your tax residency to India, they may restrict your account to "sell-only" mode or force you to liquidate your positions entirely.

- Traditional Brokers (Hargreaves Lansdown, Interactive Investor, AJ Bell): These are sometimes more flexible and may allow you to maintain a non-resident account. However, you will likely face restrictions on buying new funds, high platform fees, and you will have to manage your complex Indian tax reporting manually.

What is the best way to stay invested globally after moving back?

The best way to stay invested globally is to transfer your investments into a platform specifically built for global investing from India.

You do not need to sell your general investment account stocks just because your UK broker is restricting you. Selling triggers an actual taxable event. Instead, use an in-kind transfer. This allows you to move your entire eligible portfolio "as is" to an India-friendly platform like Paasa.

These platforms allow you to maintain your positions and trade normally, while providing India-specific compliance support and tax documents tailored for your mandatory Schedule FA reporting.

What happens to my ISA when I move back to India?

In the UK, Individual Savings Accounts (ISAs) are a fantastic wealth-building tool because all capital gains and dividends inside them are completely tax-free.

If you move abroad, your ISA (and LISA) will remain tax-free in the UK. You can keep the account open, and the investments, bonuses, and interest will continue to grow tax-free from the UK government's perspective.

However, you cannot make any further contributions to the ISA or LISA while you are a non-UK resident.

This tax-free status is not recognized by the Indian government. The moment you become a tax resident of India, all dividends and capital gains generated inside your ISA become fully taxable in India.

What's the best course of action?

Standard ISA: If you hold a standard Cash ISA or Stocks & Shares ISA, your most financially efficient option is to sell your holdings and withdraw the cash before you leave the UK.

Because you are still a UK tax resident when you execute the sale, the entire withdrawal is completely tax-free in both countries. There are no penalties or charges for withdrawing your money from these standard accounts.

Lifetime ISA (LISA): Liquidating before you leave is not automatically the best move if you hold a Lifetime ISA.

Withdrawing funds from a LISA before age 60 for any reason other than buying a qualifying first home triggers a strict 25% government withdrawal charge.

If you hold a LISA, you must take a call on whether taking a 25% penalty today makes more financial sense than leaving the account open and paying Indian taxes on its future growth over time.

What happens to my UK Pension (SIPP or Workplace) when I move back?

A common question returning NRIs have is whether they should transfer their UK pension (Workplace Pension or Self-Invested Personal Pension) back to India.

Transferring your UK pension to an Indian scheme (via a QROPS, or Qualifying Recognised Overseas Pension Scheme) is notoriously difficult and usually financially detrimental. The UK government heavily regulates these transfers, and executing one often triggers a massive "Overseas Transfer Charge" of up to 25%.

Because of this severe tax penalty, it is usually financially better to leave your pension invested in the UK. It will continue to grow tax-deferred within the UK system. You can then draw from it when you reach the eligible retirement age (currently 55, rising to 57 in 2028), at which point you simply report the income on your Indian tax returns.

Should I take my 25% tax-free lump sum before leaving?

Before you decide to simply leave your pension invested, there is one planning opportunity that is worth considering: the Pension Commencement Lump Sum (PCLS).

Under current UK pension rules, if you are aged 55 or over (rising to 57 in 2028), you can take up to 25% of your pension pot as a completely tax-free lump sum in the UK. The remaining 75% stays invested and is taxed as income when you draw it down later.

For anyone with a substantial SIPP, the timing of this decision matters:

- Taking the PCLS while still UK-resident: The lump sum is tax-free in the UK. If you also hold RNOR status in India at the time of receipt, it is tax-free there too, since foreign income received outside India is exempt during RNOR. This is the most tax-efficient scenario for eligible returning NRIs.

- Taking the PCLS after becoming a full Resident (ROR) in India: The UK still treats the 25% as tax-free. However, India's treatment of foreign pension lump sums for full residents is not clearly settled, and you lose the protection of the RNOR window.

If you are of pension access age, taking the PCLS before departure or early in your RNOR window is worth modelling carefully with a UK-qualified pension advisor.

Note: Accessing your pension, even partially, triggers the Money Purchase Annual Allowance (MPAA), which caps future pension contributions at £10,000 per year. If you have any intention of returning to the UK and contributing to a pension again, factor this in before you draw down.

tool_code

Will I be subject to UK Inheritance Tax after moving back to India?

Yes, you will still be subject to UK inheritance tax on your UK-situs assets, and potentially also on your worldwide estate, depending on the length of your UK residency.

The UK overhauled its Inheritance Tax (IHT) rules in April 2025. Under the previous system, your IHT exposure depended on your domicile.

The new system, effective from 6 April 2025, replaces this with a long-term residence test.

If you were a UK resident for more than 10 years

If you have been a UK tax resident for 10 or more of the last 20 tax years, you are classified as a "long-term resident." Under HMRC's updated IHT guidance, this means your worldwide assets remain within the UK IHT net even after you leave. Indian property, Indian stocks, and foreign bank accounts are all within scope.

This exposure does not end the moment you land in India. Depending on how many years of UK residence you accumulated, you can remain within the UK IHT net for up to 10 years after departure:

| Years of UK residence (out of last 20) | Years of IHT exposure after leaving |

|---|---|

| 10 to 13 years | 3 years |

| 14 to 16 years | 5 years |

| 17 to 19 years | 7 years |

| 20 years | 10 years |

The UK IHT rate is 40% on everything above the nil-rate band (currently £325,000, or up to £500,000 if a residential property is passed to direct descendants).

The long-term resident rules only apply if you have been a UK tax resident for 10 or more of the last 20 tax years, as determined by the Statutory Residence Test.

If you were a UK resident for less than 10 years

If you were a UK tax resident for fewer than 10 years, your non-UK assets (Indian property, Indian stocks, overseas bank accounts) are completely outside the UK IHT net.

However, five things still apply regardless of how long you were resident:

- UK property is always within scope. Residential and commercial property located in the UK is a UK-situs asset and subject to IHT at 40% above the nil-rate band, no matter where you live or how long you were resident.

- UK shares held directly are UK-situs assets. If you hold shares in UK-listed companies (FTSE stocks, for example) directly in a brokerage account, those shares remain within the IHT net. Shares held through a non-UK domiciled fund or wrapper are treated differently.

- UK bank accounts are generally in scope, with one exception: foreign currency accounts held with a UK bank are treated as excluded property for non-residents and fall outside IHT.

- The 7-year rule applies to lifetime gifts of UK assets. If you gift UK property or other UK-situs assets and pass away within seven years, those gifts can still be pulled back into your estate for IHT purposes.

- UK pensions may come into scope from April 2027. HMRC has confirmed that pension death benefits will become subject to IHT from April 2027. If you hold a SIPP or workplace pension, this is a planning consideration regardless of how long you were UK resident.

The nil-rate band is currently £325,000 per person (up to £500,000 if a UK residential property is passed to direct descendants under the Residence Nil Rate Band). Amounts above this threshold are taxed at 40%.

Tax and reporting implications of moving back to India

When you permanently return to India, your tax status eventually shifts from being a Non-Resident Indian (NRI) to a Resident.

This brings two major changes: your global income becomes taxable in India, and your reporting requirements increase significantly.

To learn more about how your global income is taxed in India and the reporting requirements, read:

- How Global Stocks and ETFs Are Taxed for Indian Investors

- Tax on Repatriation of Foreign Income to India

- Foreign Asset Disclosure (Schedule FA) Requirements for Indians

When does my UK tax residency actually end?

The UK uses a structured framework called the Statutory Residence Test (SRT) to determine this. Moving out is not sufficient on its own.

Under the SRT, the most commonly applicable automatic overseas test for returning NRIs is this: if you were a UK resident in one or more of the three preceding tax years, you become non-resident in a year where you spend fewer than 16 days in the UK.

If you spend between 16 and 45 days, the outcome is determined by tie-breakers, including whether you have a UK home available to you, whether you work in the UK, and where your family is based.

Getting this wrong by a few weeks can mean HMRC treats you as UK-resident for an additional full tax year, taxing your worldwide income accordingly.

Split year treatment

In the year you leave, HMRC does not automatically tax you as a UK resident for the full year. If you qualify, your departure year is split: a UK-resident portion and a non-resident portion. Income and capital gains arising in the non-resident portion fall outside UK tax.

HMRC's guidance on split year treatment sets out the cases under which a split year applies. For most returning NRIs leaving to settle in India, the relevant case depends on whether you are starting full-time work abroad or simply relocating. If the latter, the exact date your UK residency ends requires careful determination.

Note: The split year date determines which capital gains are within the UK tax net and which are not. If you plan to sell UK stocks or any assets held outside an ISA wrapper before returning, the timing of those sales relative to your split year date is a consequential decision. Take advice before you sell.

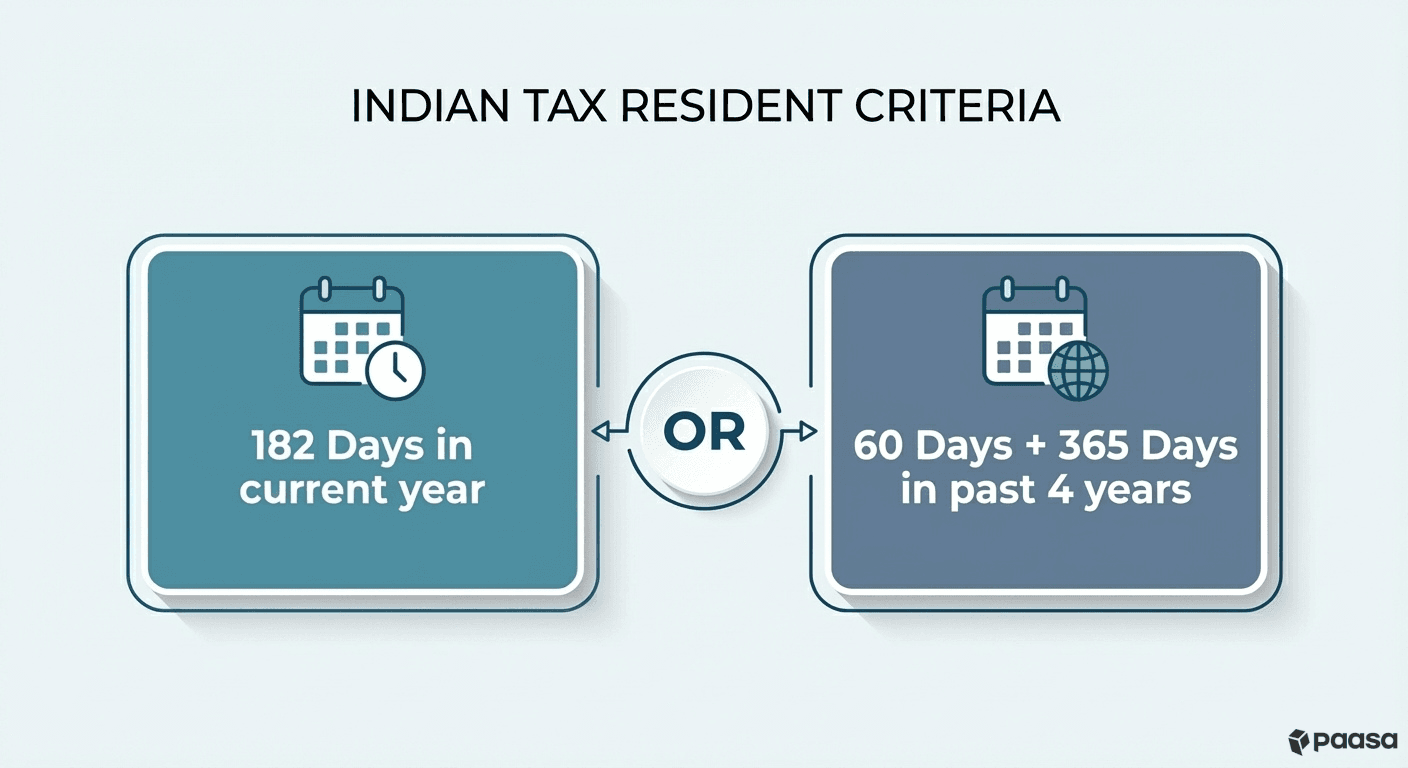

When do you become an Indian Tax Resident?

Under the Income Tax Act, you are considered a tax resident of India if:

- You are physically present in India for a period of 182 days or more in the tax year (182-day rule), or

- You are physically present in India for a period of 60 days or more during the relevant tax year and 365 days or more in aggregate in the four preceding tax years (60-day rule).

Once you meet this criterion, you are legally required to pay tax in India on income earned anywhere in the world, including UK interest, dividends, and capital gains.

What is RNOR status and how does it affect me?

RNOR (Resident but Not Ordinarily Resident) is a transitional tax residency status for returning NRIs. It functions as a bridge between being a Non-Resident and becoming a full Ordinary Resident.

You typically qualify for this status if you meet one of the following criteria:

- You have been an NRI for 9 out of the last 10 financial years.

- You have lived in India for 729 days or less in the preceding 7 financial years.

This status grants you a 1 to 3-year window where your global income is treated differently from that of a standard Indian resident.

What benefits can I get from this status?

As long as you hold RNOR status, your foreign income is NOT taxable in India, provided it is received outside India first. This allows you to manage your UK assets without immediate tax liability in India.

- Global Stocks and ETFs: If you sell assets in your general investment account while you are RNOR, the capital gains are tax-free in India.

- The ISA Tax Reset: As mentioned, you can use your RNOR window to liquidate your ISA or reset the cost basis completely tax-free before you become a full resident.

- UK Bank Interest: The interest earned in your UK bank accounts is tax-free in India.

- Dividends: Tax-free in India during this period.

To utilize these exemptions, you must receive the funds in your UK bank account first. If you wire sale proceeds or dividends directly to an Indian bank account, the income is considered "received in India" and becomes fully taxable.

Common Questions UK NRIs Have About Moving Back

Can I send money from India and buy more overseas stocks?

Yes. You can remit up to $250,000 USD equivalent per financial year under the Liberalised Remittance Scheme (LRS) to invest in foreign stocks. However, be aware that transfers exceeding ₹10 Lakhs in a year attract a 20% TCS (Tax Collected at Source), which you can claim back as a refund or tax adjustment when filing your income tax return in India.

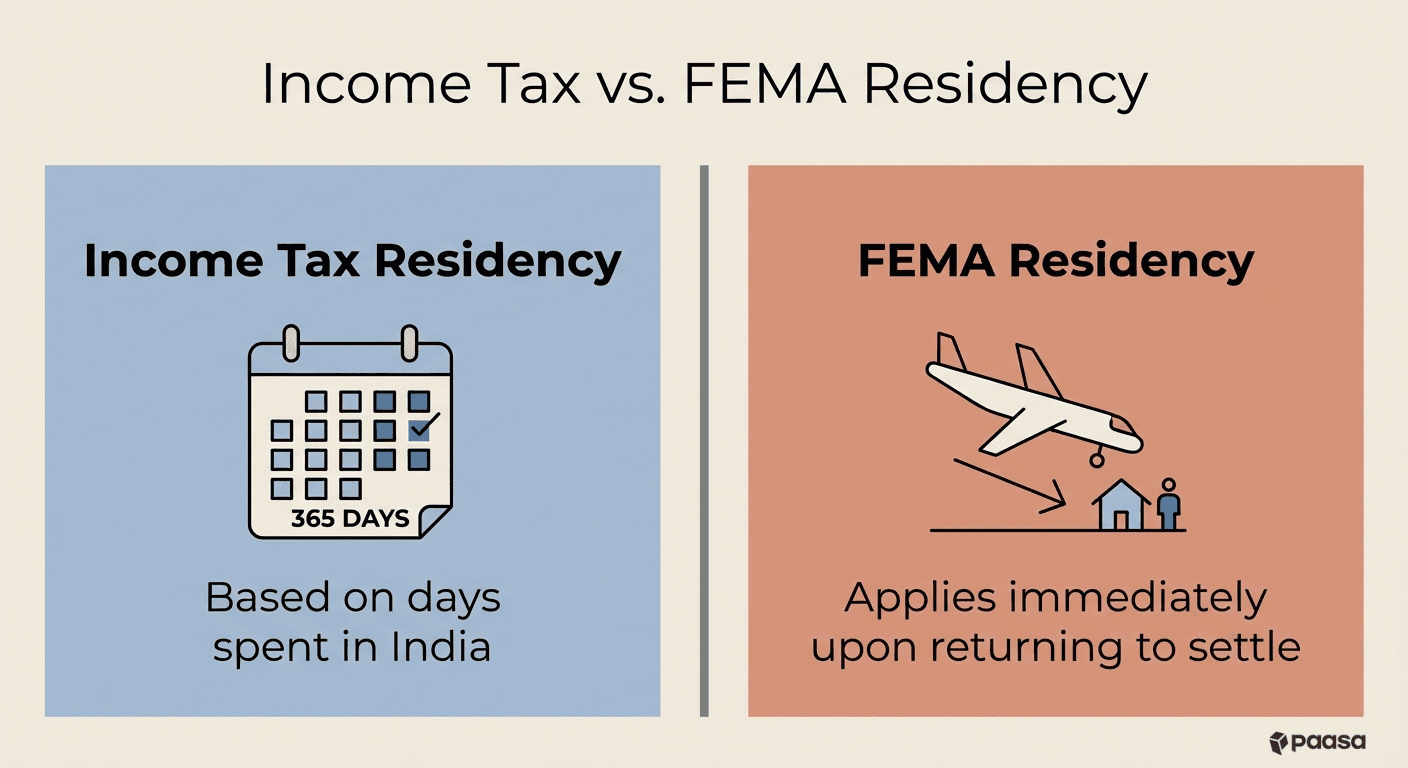

When do I become subject to FEMA upon moving back?

You become a resident under FEMA immediately upon landing in India if your intention is to stay for an uncertain period or for employment and business. Unlike income tax residency (which counts days), FEMA residency applies the moment you return to settle.

Can I continue operating my UK bank account?

Yes. Section 6(4) of FEMA allows you to continue holding and operating foreign bank accounts, stocks, and properties if they were acquired when you were a resident outside India. You are not legally required to close your Barclays, Monzo, or HSBC UK accounts.

Can I keep my NRO account?

No. Once your status changes to Resident, you are legally required to inform your bank and convert your NRO account to a standard Resident Savings Account. Continuing to hold an NRO account as a resident is a violation of FEMA regulations.

About Paasa

Paasa is a global investing platform built specifically for Indian residents and returning NRIs. We provide direct access to over 10 global exchanges and support 9 global currencies, allowing you to build a truly international portfolio.

- Seamless In-Kind Transfers: You can move your entire global stock portfolio directly to Paasa. This allows you to consolidate your assets in one place without triggering a tax event.

- The Compliance Advantage: Paasa provides the exact reports you need for your Indian tax returns and foreign asset disclosures, eliminating the need for manual calculations.

- Estate Tax Protection: Paasa offers access to Ireland-domiciled (UCITS) ETFs, allowing you to legally shield your investments from the US Estate Tax if your portfolio includes US equities.