Indian professionals who are moving back from Australia often lack clarity about how they can manage their overseas holdings like stocks, ETFs, Superannuation account, and RSUs after moving back.

This article explains how you can manage your overseas holdings after moving back to India and navigate ATO's "deemed disposal" exit tax.

We also cover your new Indian tax and reporting requirements, your changing tax residency status, and RNOR rules and opportunities.

Table of contents

- What happens to my stocks when I move back to India?

- What happens to my Superannuation when I move back to India?

- What happens to my RSUs and stock options when I move back?

- What happens to my Australian property when I move back?

- When does my Australian tax residency actually end?

- Tax and reporting implications of moving back to India

- What is RNOR status and how does it affect me?

- Common Questions NRIs Have About Moving Back from Australia

- About Paasa

What happens to my stocks when I move back to India?

When you move back to India, the first major hurdle you face is the Australian exit tax, known as "Deemed Disposal."

Deemed disposal is a unique facet of the Australian tax system that treats your assets as disposed of at their current market value when you become a non-resident for tax purposes, whether you have actually sold them or not.

It occurs on the day you cease to be an Australian resident for tax purposes and triggers a tax event that may result in a capital gain or loss.

Practically, this means you either have to sell a portion of your portfolio to pay the resulting tax bill, or you have to pay the taxes on these "paper profits" out of your own pocket to keep your positions open.

Does deemed disposal apply to all my assets?

Deemed disposal applies to all CGT assets, with the exception of "taxable Australian property" (like physical real estate in Australia, which remains taxable there until you actually sell it).

In case of assets bought before your Australian residency (for example, US stocks or ETFs acquired before you moved to Australia), the ATO only taxes the gains that occurred while you were a resident.

Three things you need to know about the exit tax:

1. The 50% CGT discount applies.

If you have held an asset for more than 12 months before your departure date, only 50% of the capital gain is included in your taxable income. This is the most important planning detail for anyone with a long-held portfolio. An investor with AUD 500,000 in unrealised gains on shares held for over a year pays CGT on AUD 250,000, not the full amount.

2. Pre-residency assets have a reset cost base.

For assets you acquired before you first became an Australian tax resident, the ATO resets your cost base to the market value on the day you became an Australian resident. You are only taxed on gains that accrued during your period of Australian residency, not on appreciation from before you arrived.

3. You can defer the deemed disposal.

You have the option to disregard the capital gain triggered by deemed disposal and instead treat those assets as if they were Australian property until you actually sell them. If you make this choice, Australian CGT continues to apply when you eventually sell, but you pay nothing upfront at departure.

What happens to the assets I choose to keep?

Under Indian FEMA regulations, you are legally allowed to indefinitely hold any foreign stocks, ETFs, or properties you acquired while living abroad. You do not have to sell them just because you moved.

However, while Indian law allows you to keep them, Australian platforms and specific investment products might not:

- Retail Brokers (Stake, Pearler, Superhero): These platforms generally cater strictly to Australian residents. When you become an Indian resident, they may restrict your account or force you to liquidate your positions immediately.

- Traditional Brokers (CommSec, Nabtrade): These are more flexible and may allow you to maintain a non-resident account with some restrictions. However, you will have to manage your Indian tax reporting manually.

- Managed Funds: Certain unlisted Australian managed funds explicitly prohibit non-resident unitholders. If you hold these, you will need to redeem your units when you leave the country.

What's the best way to stay invested globally after moving back to India?

The best way to stay invested globally is to transfer your investments into a platform specifically built for global investing from India.

These platforms allow you to maintain your positions and trade normally, while providing India-specific compliance support and tax documents tailored for your mandatory Schedule FA reporting.

What happens to my Superannuation when I move back to India?

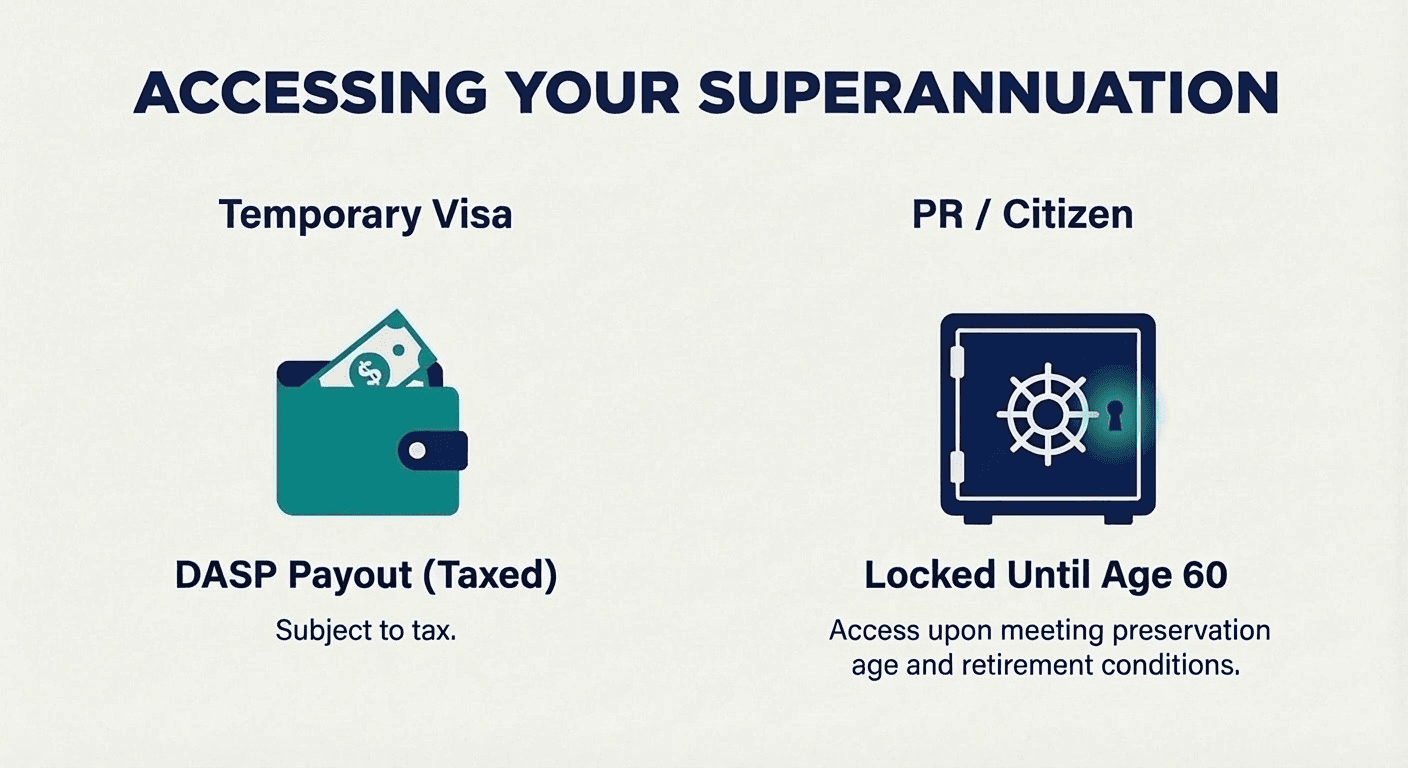

What happens to your Superannuation when you leave Australia depends on your visa status:

- Temporary Visa Holders: If you were on a temporary working visa (like a 482), you can claim your Super after you leave Australia and your visa expires. This is called a Departing Australia Superannuation Payment (DASP). Note that this payout is taxed (typically between 35% and 65% depending on the components).

- Permanent Residents and Citizens: You cannot withdraw your Superannuation just because you are leaving. Your money stays locked in Australia until you reach your preservation age and retire (usually 60).

How India treats your Super

If your Super stays in Australia, the fund continues to pay 15% tax on earnings inside the fund. Once you become a full Indian tax resident (ROR), those earnings are also taxable in India. You declare them in your Indian tax return and claim a foreign tax credit for the 15% already paid by the Australian fund, so you pay the difference rather than the full amount twice.

During your RNOR window, earnings inside the fund are foreign income and are not taxable in India, giving you a period of shelter.

The RNOR planning opportunity for eligible withdrawals.

If you are aged 60 or over, you have reached your preservation age and can access your Super by satisfying a condition of release. Withdrawals from a taxed Super fund made by someone aged 60 or over are completely tax-free in Australia.

During your RNOR window in India, a Super withdrawal received in your Australian bank account is also not taxable in India, since foreign income is exempt during RNOR. This makes the RNOR window the most tax-efficient time to make Super withdrawals if you are eligible. Once you become a full ROR, Super withdrawals may become taxable in India depending on the circumstances.

Note: The India-Australia DTAA treatment of Super withdrawals for Indian residents is not entirely settled in practice. Confirm the applicable position with a tax advisor before drawing down significant amounts after your RNOR period expires.

What happens to my RSUs and stock options when I move back?

If you worked at an Australian company or a multinational with Australian operations, you likely hold RSUs or stock options through an Employee Share Scheme (ESS). Moving back to India mid-vesting period has specific tax consequences you need to plan for.

How RSUs are normally taxed in Australia

RSUs under a standard ESS deferral scheme are taxed at the deferred taxing point, which is usually the date your vesting conditions are met and the shares are transferred to you. At that point, the market value of the shares is included in your assessable income and taxed at your marginal rate, just like salary.

What changes when you leave mid-vesting period

Leaving Australia does not automatically trigger a taxing event on your unvested RSUs. However, when those RSUs eventually vest after you have left, only the portion of the income that relates to your Australian employment is taxable in Australia.

As a foreign resident, you only pay Australian income tax on ESS income to the extent it relates to employment performed in Australia. The Australian-source portion is calculated by dividing your Australian workdays during the full vesting period by your total workdays during that period.

Example

You have a 4-year RSU grant. You worked in Australia for 3 of those 4 years and returned to India for the final year. At vesting, the shares are worth AUD 200,000.

| Component | Amount | Note |

|---|---|---|

| Total RSU income at vesting (A) | AUD 200,000 | Market value on vest date |

| Australian workdays in vesting period (B) | 75% | 3 years out of 4 |

| Australian-source income (A × B) (C) | AUD 150,000 | Taxable in Australia |

| Indian-source income (A minus C) (D) | AUD 50,000 | Not taxable in Australia |

| Australian tax at ~47% top marginal rate on (C) | ~AUD 70,500 | Top marginal rate plus Medicare levy |

During your RNOR window in India, the Australian-source portion is foreign employment income and is not taxable in India. Once you become a full Resident (ROR), it becomes taxable at your slab rate, with a foreign tax credit available for the Australian tax already withheld.

Note: Keep a workday log from the grant date of every RSU through to vesting. Your employer's payroll team should track this, but verify the apportionment is correctly applied. The calculation covers the entire vesting period from grant, not just from the date you moved back.

What happens to my Australian property when I move back?

Australian real estate is excluded from the deemed disposal exit tax, so you do not pay a departure tax when you leave even if the property has appreciated significantly. You can continue to hold it. However, two obligations apply once you become a non-resident.

Rental income as a non-resident

If you rent out your Australian property after leaving, you remain taxable in Australia on that rental income and must lodge an Australian tax return each year to declare it. Australian rental income for non-residents is taxed at foreign resident rates, which start at 32.5% with no tax-free threshold. You can deduct allowable expenses including mortgage interest, property management fees, repairs, and depreciation.

How does India treat this rental income?

This depends on your Indian residency status:

- During RNOR: Rental income from your Australian property is tax-free in India, provided it is received in your Australian bank account first. If it is wired directly to your Indian account, it becomes taxable in India immediately. To learn more, read our guide on foreign rental income for RNORs.

- After becoming ROR: India also taxes the rental income at your slab rate. Under the India-Australia DTAA, Australia retains primary taxing rights on rental income from Australian property. India gives you a foreign tax credit for the Australian tax already paid, so you do not pay tax on the full amount twice.

Example

You rent your Sydney property for AUD 4,000 per month (AUD 48,000 per year). Your deductible expenses are AUD 15,000. You are in the 30% Indian tax slab with income above ₹2 crore.

| Component | RNOR year | ROR year |

|---|---|---|

| Gross rental income | AUD 48,000 | AUD 48,000 |

| Australian deductible expenses | AUD 15,000 | AUD 15,000 |

| Australian taxable income | AUD 33,000 | AUD 33,000 |

| Australian tax at 32.5% on net (A) | AUD 10,725 | AUD 10,725 |

| Indian base tax at 30% on gross (B) | Nil | AUD 14,400 |

| Surcharge at 25% of (B) (C) | Nil | AUD 3,600 |

| Cess at 4% of (B+C) (D) | Nil | AUD 720 |

| Gross Indian tax (B+C+D) | Nil | AUD 18,720 |

| Foreign tax credit for (A) | N/A | AUD 10,725 |

| Net Indian tax payable | Nil | AUD 7,995 |

| Total tax paid | AUD 10,725 | AUD 18,720 |

Selling Australian property as a non-resident

When you sell Australian property as a non-resident, the buyer is required to withhold 15% of the gross sale price under the ATO's Foreign Resident Capital Gains Withholding (FRCGW) rules (for contracts signed on or after 1 January 2025) and remit it to the ATO. This withholding is on the full sale price, not on your gain. You recover the excess by lodging an Australian tax return for the year of sale.

If your actual CGT liability is lower than the 15% withheld, you can apply for a variation notice before settlement to reduce the withholding rate.

Which country taxes the gain, and when?

Under the India-Australia DTAA, Australia has primary taxing rights on gains from Australian real estate regardless of where you live.

- During RNOR: The gain is completely exempt in India. Only Australia taxes the sale. This is the most efficient window to sell if you are planning to anyway.

- After becoming ROR: India also taxes the gain at 12.5% LTCG (for property held over 24 months, under post-2024 budget rules). India gives you a foreign tax credit for the Australian tax paid. For most of our readers with significant gains, the Australian tax will exceed India's 12.5% LTCG liability, meaning no additional Indian tax is owed in practice. Confirm your specific position with a CA before the sale.

Note: If you are still an Australian tax resident at the time of sale, you need an ATO clearance certificate to avoid the buyer withholding 15%. Apply for it well before settlement as it takes up to 28 days to process.

When does my Australian tax residency actually end?

Moving back to India does not automatically end your Australian tax residency. The ATO uses a facts-and-circumstances approach, and there is no single formal deregistration step you can take.

The ATO applies four residency tests. The primary one for returning NRIs is the domicile test: you are considered an Australian resident if your domicile is in Australia, unless the ATO is satisfied your permanent place of abode is outside Australia. This is assessed holistically based on factors including your intention to remain in India, whether you have a settled home there, your family ties, and whether you have genuinely severed your connections to Australia.

The ATO also applies a 183-day test: if you spend more than 183 days in Australia in a financial year, you remain a tax resident for that year unless your usual place of abode is outside Australia and you have no intention of taking up residence here. For returning NRIs who visit Australia frequently to see family or manage property, this is a live risk worth tracking.

To get the ATO's formal view on your residency status, use their Determination of Residency Status tool. Practical steps that support a clean break include: establishing a settled home in India, reducing Australian financial ties, notifying your Australian employer and bank of your status change, and staying under 183 days in Australia in the year of departure.

What do I need to file with the ATO when leaving?

Departure year tax return

You must lodge an Australian tax return covering the period from 1 July to the date you ceased being an Australian resident. This return reports your income for the Australian-resident portion of the year and declares any CGT arising from deemed disposal. You can lodge this early before the standard 31 October deadline if you want to finalise your Australian tax affairs before leaving.

Ongoing filing obligations

Once you are a non-resident, you still need to lodge an Australian tax return for any year in which you have Australian-source income that is not subject to final withholding tax. This includes rental income from Australian property and capital gains from selling Australian property. Australian interest, dividends, and royalties are generally subject to non-resident withholding tax as a final tax and do not require a return.

If you no longer have any Australian-source income requiring a return, notify the ATO by lodging a non-lodgment advice. This keeps your ATO record clean and stops reminders from being issued.

Tax and reporting implications of moving back to India

When you permanently return to India, your tax status eventually shifts from being a Non-Resident Indian (NRI) to a Resident.

This brings two major changes: your global income becomes taxable in India, and your reporting requirements increase significantly.

To learn more about how your global income is taxed in India and the reporting requirements, read:

- How Global Stocks and ETFs Are Taxed for Indian Investors

- Tax on Repatriation of Foreign Income to India

- Foreign Asset Disclosure (Schedule FA) Requirements for Indians

When do you become an Indian Tax Resident?

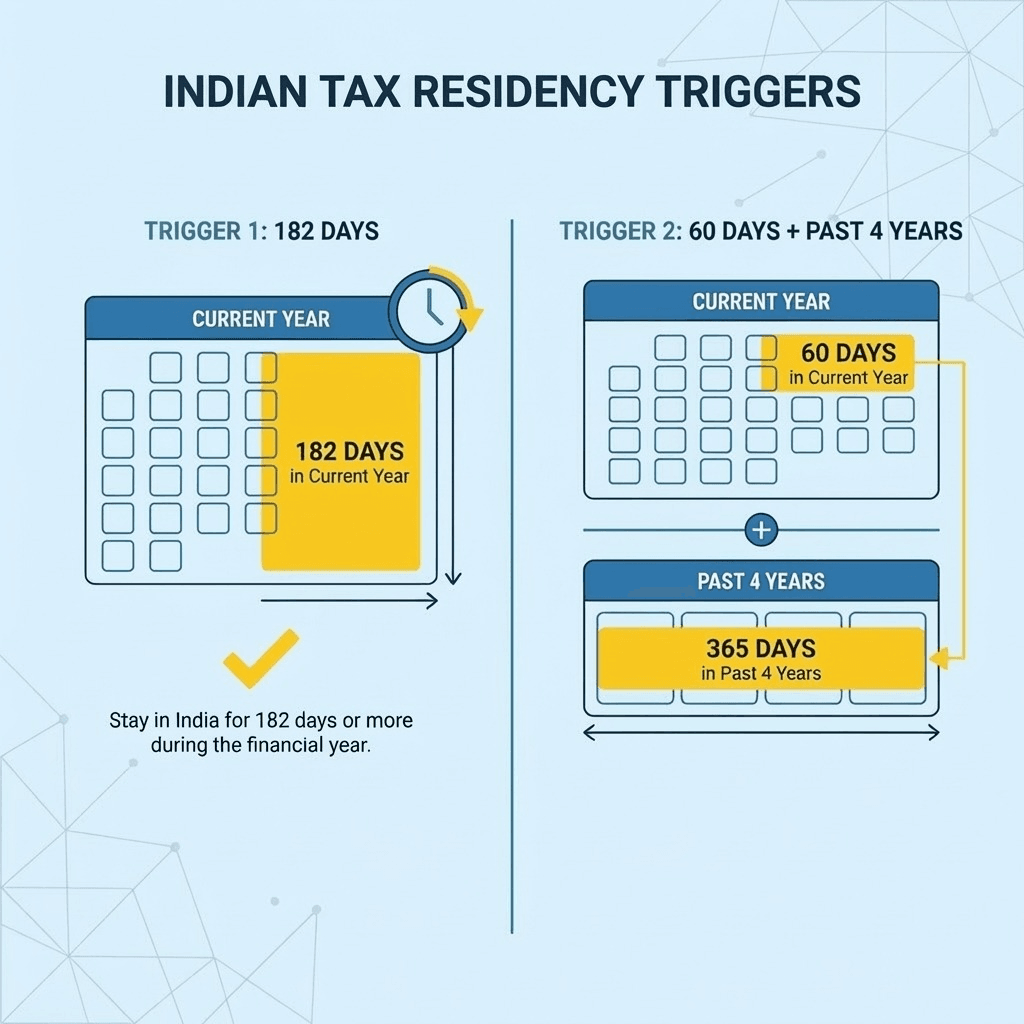

Under the Income Tax Act, you are considered a tax resident of India if:

- You are physically present in India for a period of 182 days or more in the tax year (182-day rule), or

- You are physically present in India for a period of 60 days or more during the relevant tax year and 365 days or more in aggregate in the four preceding tax years (60-day rule).

Once you meet this criterion, you are legally required to pay tax in India on income earned anywhere in the world, including Australian interest, dividends, and capital gains.

What is RNOR status and how does it affect me?

RNOR (Resident but Not Ordinarily Resident) is a transitional tax residency status for returning NRIs. It functions as a bridge between being a Non-Resident and becoming a full Ordinary Resident.

You typically qualify for this status if you meet one of the following criteria:

- You have been an NRI for 9 out of the last 10 financial years.

- You have lived in India for 729 days or less in the preceding 7 financial years.

This status grants you a 1 to 3-year window where your global income is treated differently from that of a standard Indian resident.

What benefits can I get from this status?

As long as you hold RNOR status, your foreign income is NOT taxable in India, provided it is received outside India first. This allows you to manage your Australian assets without immediate tax liability in India.

- Global Stocks & ETFs: If you sell them while you are RNOR, the capital gains are tax-free in India. (Note: You still need to account for your Australian tax obligations based on the exit tax).

- Australian Bank Interest: The interest earned in your Australian accounts is tax-free in India.

- Dividends: Tax-free in India during this period.

- Superannuation Protection: Any growth or income generated within your Super fund is not taxed by India during your RNOR window.

To utilize these exemptions, you must receive the funds in a overseas bank account first. If you wire sale proceeds or dividends directly to an Indian bank account, the income is considered "received in India" and becomes fully taxable.

Common Questions NRIs Have About Moving Back from Australia

Can I send money from India and buy more overseas stocks?

Yes. You can remit up to $250,000 USD equivalent per financial year under the Liberalised Remittance Scheme (LRS) to invest in foreign stocks. However, be aware that transfers exceeding ₹10 Lakhs in a year attract a 20% TCS (Tax Collected at Source), which you can claim back as a refund or tax adjustment when filing your income tax return in India.

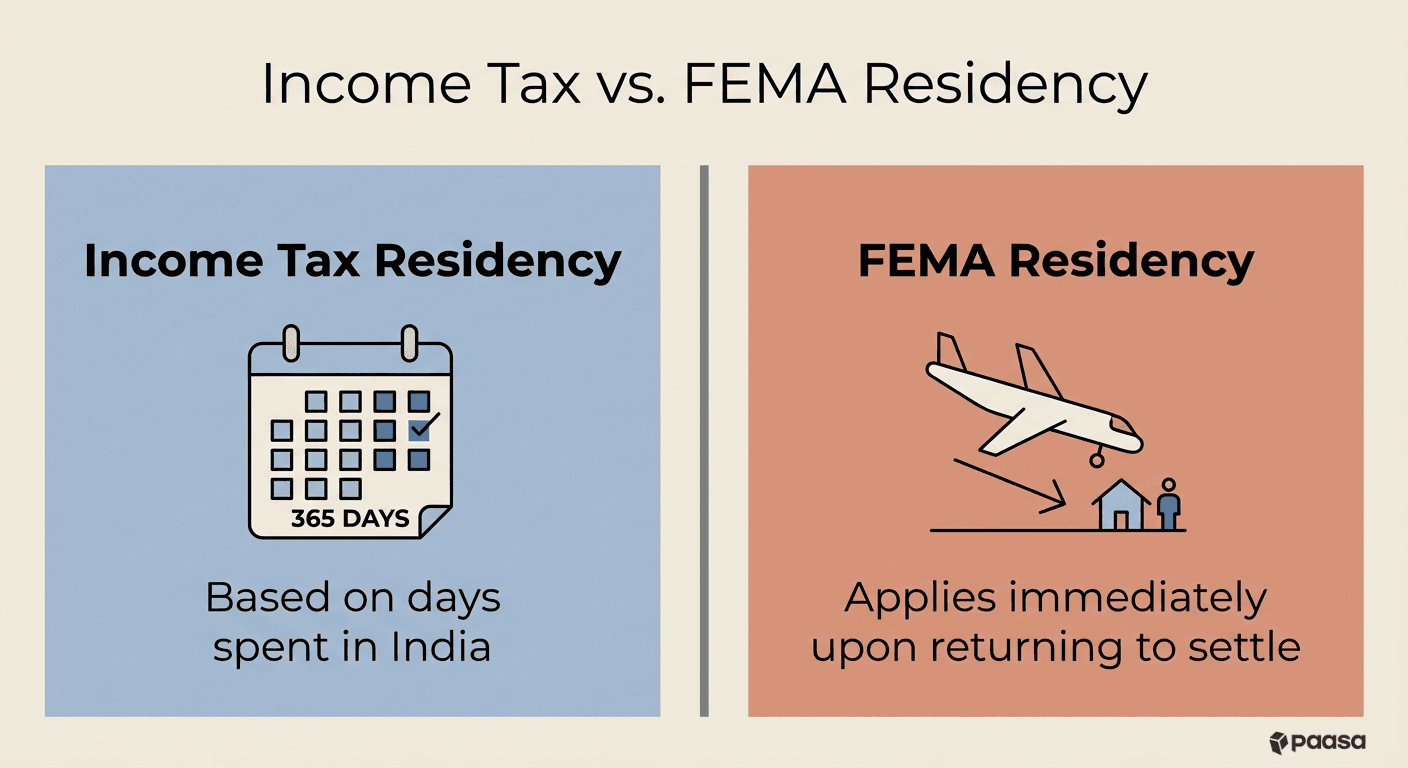

When do I become subject to FEMA upon moving back?

You become a resident under FEMA immediately upon landing in India if your intention is to stay for an uncertain period or for employment and business.

Unlike income tax residency (which counts days), FEMA residency applies the moment you return to settle.

Can I continue operating my Australian bank account?

Yes. Section 6(4) of FEMA allows you to continue holding and operating foreign bank accounts, stocks, and properties if they were acquired when you were a resident outside India. You are not legally required to close them.

Can I keep my NRO account?

No. Once your status changes to Resident, you are legally required to inform your bank and convert your NRO account to a standard Resident Savings Account. Continuing to hold an NRO account as a resident is a violation of FEMA regulations.

About Paasa

Paasa is a global investing platform built specifically for Indian residents and returning NRIs. We provide direct access to over 10 global exchanges and support 9 global currencies, allowing you to build a truly international portfolio.

- Seamless "In-Kind" Transfers: You can move your entire global stock portfolio directly to Paasa. This allows you to consolidate your assets in one place without triggering a tax event.

- The Compliance Advantage: Paasa provides the exact reports you need for your Indian tax returns and foreign asset disclosures, eliminating the need for manual calculations.

- Estate Tax Protection: Paasa offers access to Ireland-domiciled (UCITS) ETFs, allowing you to legally shield your investments from the US Estate Tax if your portfolio includes US equities.